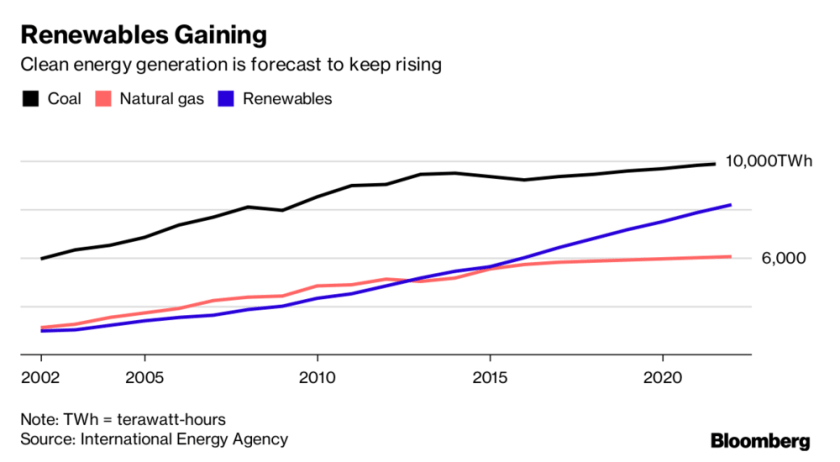

Europe is decreasing CO2 emissions. The United States not so much. And the Europeans will find it difficult to meet their Paris treaty commitment. [The Economist July 8, 2017]

The accompanying chart is relevant but murky.

The chart baseline is 1997, but the treaty reference is 1990. There appears to be little difference between the EU and the US on this scale. China appears to have a huge output but is not mentioned in the article.

Charts that show percent changes from a year are common in finance but can be questionable. Why was that year chosen? Is it representative? Are the series close enough in scale that the comparison makes sense?

The data look like

This graph makes it clearer that the EU is decreasing emissions faster than the US. Also China is clearly not going to achieve a 40% reduction from 1990, but its output is only about twice the US—rather less dramatic than suggested in the original chart.

Data from

Statistics Explained (http://ec.europa.eu/eurostat/statisticsexplained/) – 16/06/2017 and

Source: Boden, T.A., Marland, G., and Andres, R.J. (2017). National CO2 Emissions from Fossil-Fuel Burning, Cement Manufacture, and Gas Flaring: 1751-2014, Carbon Dioxide Information Analysis Center, Oak Ridge National Laboratory, U.S. Department of Energy, doi 10.3334/CDIAC/00001_V2017